Quick Jump

Document Repository

Why Now

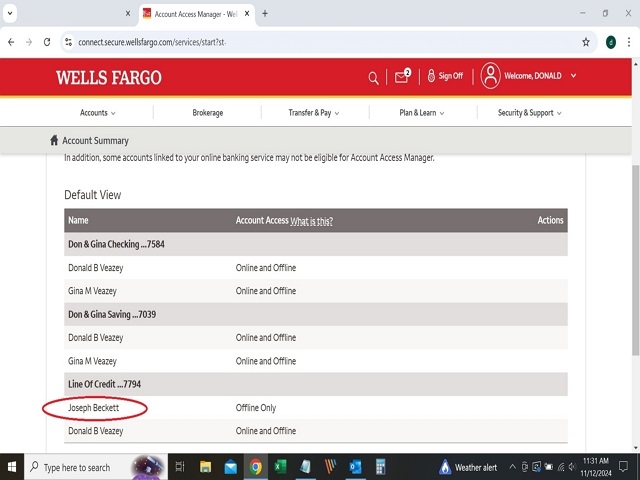

November 11, 2024, my wife Gina and I were reviewing her business accounts at Wells Fargo as

part of her annual tax planning. She was unable to access her Line of Credit (LoC). Confused,

we switched users, as I knew I had access to that account.

To our shock, my wife gasped, "What the hell!". When I looked at the security screen, I

realized this was yet another instance of harassment by Thomas DuBreuil, a former Wells

Fargo employee that I've had issues with in the past.

Mr. Joseph Beckett had been granted walk-in access to my wife's business account.

Mr. Beckett is known to me as my estranged stepbrother and a companion of Thomas DuBreuil.

I contend that the court order dated June 21, 2011, issued by Judge Ayvazian, contained a fundamental error. This order,

which granted an unrelated individual access to a private business account, was requested by Attorney Ad Litem Sharp,

representing my mother. I assert that the court lacked the jurisdictional authority to issue such an order. It appears

that Attorney Ad Litem Sharp, in presenting this request, was misled and lacked the requisite skillset to fully

comprehend the implications.

Federal Law: 18 U.S.C. § 1344 (Bank Fraud) criminalizes knowingly executing, or attempting to execute, a scheme or artifice

to defraud a financial institution. The act of deceiving the bank into adding an unauthorized party to an account,

often by making a false claim of ownership/consent, falls under this category.

Moreover, Attorneys Thomas and Karsnitz escalated this deception into criminality, further misleading the courts of

Delaware. They achieved this by integrating a fabricated document supplied by guardian and by false representation

of "Waiver of Appearance" requested of me by Karsnitz.

I have compiled the relevant supporting documentation for these assertions. Given that the initial order was issued

by a judge, it is imperative that we seek judicial correction through the appropriate channels.

From: don@elysiumeast.com

Sent: Tuesday, November 12, 2024 11:45 AM

To: 'Gina Veazey'

Subject: Unauthorized User on Wells Fargo LOC - Security Breach

Gina,

I am deeply concerned about the recent security breach involving the unauthorized addition

of a user to the business LOC account. I understand that you discovered this breach while using

my login credentials and was truly surprised to understand you had no access.

This incident highlights a significant security vulnerability in our systems. I will immediately

initiate a comprehensive review of our security protocols to identify any weaknesses and implement

necessary measures to prevent future occurrences.

While I understand the need for your management access to the LOC, and we could potentially

remove Mr. Beckett, both using my login, I believe that overriding the judge's order might not be

feasible. To ensure we take the most appropriate steps to protect our interests, I recommend that

we consult with an attorney. An attorney can provide expert legal advice and guidance on the best

course of action, considering the specific circumstances and legal implications.

I will initiate the process of securing legal counsel immediately. Please let me know if you

have any specific questions or concerns.

Thank you for bringing this serious matter to my attention.

Don

Background

My parents were local real estate investors. My mother, Alberta, discussed investments with her

Wachovia stockbroker, Rick Model, and often chatted with customer service rep Mr. DuBreuil

while waiting.

After my father's death, I assumed control of my mother's finances via power of attorney.

I liquidated and closed my parents' old Wachovia investment accounts. At my mother's request,

I set up a family gifting trust for her three children: Bob, Jack, and myself.

I created a $285,000 irrevocable trust ($100,000 +-

for each child), consulting with attorney John Ryan. Often called a Medicaid trust is a

legal tool that allows individuals to protect their assets while still qualifying for Medicaid

benefits, particularly for long-term care.

John Ryan, is not only an attorney but also a CPA, a Certified Financial

Planner, and a Chartered Financial Analyst. Mr. Ryan provided comprehensive financial,

gifting, tax, and senior living planning. All trust documents were drafted in Virginia

and executed in Delaware. As directed by Mr. Ryan working w/Judy V at nationwide to ensure it

was titled correctly, a Nationwide annuity was retitled from Alberta Veazey to Don Veazey,

Annuitant, who would receive any payout on behalf of the trust, as per Mr. Ryan's instructions.

Mom's house was also retitled to the trust, also as per Mr. Ryan's instructions.

Analyst Commentary:

SSC eFile "Business Entity Details E Alberta Veazey Family LLC" June 30, 2009.

The mesothelioma Lawsuit

My mother, Alberta Veazey, and I pursued a mesothelioma lawsuit based on my father's wrongful death.

She received $1.3 million as the surviving spouse, the bulk disbursed throughout 2009, as we completed 13 individual

settlements encompassing both her claim and the wrongful death claim. My portion of the settlement,

as a surviving child, was less than hers.

Analyst Commentary: August 25 2008 DURABLE POWER OF ATIORNEY

KNOW ALL MEN BY THESE PRESE, THAT I, E. ALBERTA VEAZEY, of Sussex

County, Delr.ware, do hereby make, constitute, and appoint my sons, DONALD B. VEAZEY and

JOSEPH J. BECKETT, either of whom may act independently of the other

My mother asked me to transfer $418,000 to each of my step-brothers, Bob and Jack, then

$39,666 to Bob, Jack & myself. To facilitate these transfers and provide a clear record,

I retained an attorney, Mr. Ryan to draft a

Memorandum of Understanding detailing the source (Alberta Veazey) and purpose (gift) of the funds.

The total transfer amount was to be $1 million. At the time, the FDIC limit was $250,000 per account. In

addition to mom's existing money market account, I opened three additional money market

accounts, to ensure full insurance coverage mitigating any potential risk.

My Encounters With DuBreuil

My first encounter with Mr. DuBreuil (June 2009) involved opening a simple trust checking

and money market account at Wachovia. I gave him the benefit of the doubt and the respect my

parents had shown him. Initially, everything seemed fine. While not particularly bright, he

was competent enough to handle simple banking tasks. For example, assisting me with

obtaining an EIN for the trust was without issue.

Then the problems with DuBreuil started. It was a simple request -

Put one check

in Alberta's money market:

June 24, 2009

DuBreuil then decided to move the money to the Trust, splitting between trust's checking and savings accounts.

DuBreuil first deposition mesothelioma settlement

payout misunderstanding and the Trust

DuBreuil states in email:

The

checks you deposited in Mom's money market

cleared. The total deposit was $16,235.36.

I took 1/2, ($8117.68), and split between the 2 new accounts I opened for you yesterday.

All checks related to the settlement are to go into these accounts

. Acct ending in 3332 is the checking account, and the other

one ending in 3345 is the money market. Bank regulations limit withdrawals from this acct

to 3 per month. When you are ready to order checks for the checking acct let me know.

Keep in touch if you need anything.

Sincerely yours,

Thomas R. DuBreuil

Sr.Licensed Financial Specialist

Rehoboth/Lewes Financial Center

18489 Coastal Hwy, DE5819

Rehoboth Beach, DE 19971

Tel 302-644-2733,Fax 302-644-6353

I correct him:

June 24, 2009

Tom,

We agreed we would populate the LLC accounts with $100 each, so I'm puzzled

by the unauthorized move of $16,235.36.

As you know, I'm managing the entirety of my mom's finances. Though the

proceeds from the lawsuit are a significant part, there's a bigger

picture...

It's "birthday season" at the Veazey's. Bob has been given $10,000, and Don

and Jack have been given $5,000. Per mom's instruction, I will be writing

two checks for $5,000 each to Jack and me, respectively, on Friday, June

26, on account ending in 5821. This will ensure each boy is given $10,000

for the year. The deposit of $16,235.36 was to cover those disbursements.

I'm concerned that you have moved the $16,235.36 deposit into the LLC

without my consent, as I would appropriately be for any deposit of any

amount, but now I'm also concerned about covering the checks my mom has

asked me to write this week. I hope you can help with the latter by

reversing the unauthorized transaction.

Finally,

I'm concerned that there may be a fundamental misunderstanding

regarding how to handle proceeds from the lawsuit. In talking to John Ryan,

it was my understanding that it would be advantageous to my mother and the

family to accumulate funds for disbursement to the three boys outside of

the LLC, with the remainder moved to the LLC at a later date.

By copy of this e-mail, I am asking John to confirm. Please feel free to

ask any questions you may have of John. I'll be away from my desk all day

Wednesday, so I hope the two of you will communicate as necessary, copying

me.

Thanks for your assistance,

Don Veazey

This was also corroborated by attorney, Mr. Ryan.

June 24, 2009 DuBreuil responds:

I am sorry for the misunderstanding. It is not my practice to act unilaterally, but only per

the instructions of my clients.

I do remember us having a conversation regarding the placing

of lawsuit funds into the LLC account, and my understanding was that that is where they would be

placed. I honestly thought I was acting as we had agreed. I will move the money, less the

$100 for each account, back to Alberta's money market this morning. I will also call John [Ryan] and

discuss with him the best way to handle disbursements from the lawsuit., then e-mail you back the

results of the conversation copying John as you had requested.

My thought process in recommending using the LLC account for collection and disbursment of

the assets from the lawsuit is based upon past experience with these types of situations.

Although each situation is unique, it is common that assets flow into and out of accounts

that are titled for that purpose such as the LLC account I have set up. Control and tax

reporting are common benefits for handling the assets in this manner.

Analyst Commentary: DuBreuil demonstrates his incorrect understanding of Alberta and Don's mesothelioma settlement,

believing all mesothelioma settlements must go to a trust "overseen" by him. Upon final settlement, he was asked to disburse

these funds. He states in evidence he then did distribute a portion of these funds to Bob & Jack Beckett. Bob & Jack Beckett

did not participate in the mesothelioma action for lack of standing. DuBreuil did not understand the funds he disbursed were

Alberta's personal funds, gifted to Bob & Jack to compensate for their non-participation in the mesothelioma settlement.

This directly led to accusations of theft by Karsnitz to the courts of Delaware, accusations of estate mismanagement by

Sharp to the courts of Delaware, and civil litigation in Virginia.

The DuBreuil Hallucinations

In the above email, DuBreuil firmly established his belief that all of Alberta's mesothelioma disbursements would be deposited

into the trust. Later, in

deposition testimony, DuBreuil referred to Wells Fargo Bank's usual practices. DuBreuil then delusionally

stated his belief that on October 15, 2009, he withdrew one million dollars from the

Gifting Trust account(s) and distributed it

to the three family members.

DuBreuil attempted to explain the trust to Jack. DuBreuil and Jack went together to Wells Fargo Bank. At the bank,

they discovered four accounts receiving Alberta's mesothelioma disbursements, but these accounts were closed shortly

after being opened. They found approximately two dozen deposits, including a single deposit for

$427,833.32. DuBreuil explained to Jack that this paticular deposit represented

Alberta's share of the mesothelioma disbursements and asserted that "she has plenty of money." DuBreuil then concluded

that Don moved this money to an account Don solely controlled and, as stated in e-mail to Jack's attorneys Thomas and Karsnitz,

[Don is] "refusing all requests to release these funds to Jack for the care of his mother in long-term care."

Don's attorneys are baffled by these assertions.

Analyst Commentary: This is a common sales tactic: "You're losing money right now – if you move management to me,

I will reverse that." Then, a quick pivot: "Now, what does retirement look like to you? I'd like to suggest an income stream.

How much are you receiving from Social Security?... So you would need $$$ more. Well, I have a product..."

The goal is to let the thought of losing money fester, while distracting the client with aspirational retirement questions.

Only then does the glossy sales brochure appear.

Finally, the 30% commission. Where does that commission actually come from?

DuBreuil's First Deposition and Worldview of the Veazey mesothelioma Lawsuit

MR. MASSELI: Q Now, does this correctly reflect an understanding you had that the

proceeds from the

mesothelioma lawsuit were going to be placed in the LLC?

A You know, I honestly don't -- I honestly don't remember specifically that...

later in deposition:

MR. MASSELI: Q And do you recall what this transfer was about?

A ... So that is the correction that Don had asked me to make to correct my misunderstanding.

At this time DuBreuil was only peripherally familiar with

Qualified Miller Trusts and didn't understand the complexity of

actual estate planning.

Mr. Masselli: Q Are you familiar with

the term Medicaid trust?

Mr. DuBreuil: A Yes. Well, Medicaid trust, and I'm familiar with what they call Qualified Miller Trusts...

Key Differences: Medicaid Trusts vs. Qualified Miller Trusts

Medicaid Trusts (Asset Protection Trusts):

These trusts primarily address asset limitations. They are designed to protect assets from being

counted towards Medicaid's asset eligibility requirements. They are often used for long-term

planning to preserve assets for heirs. These trusts are very complex and there is a 5 year look

back period to be aware of.

Qualified Miller Trusts (Qualified Income Trusts):

These trusts address income limitations. They are specifically for individuals whose income

exceeds Medicaid's income limits. They allow excess income to be deposited into the trust,

which is then used for medical expenses. They are primarily used to qualify for Medicaid in

"income cap" states.

DuBreuil Becomes Angry

June 2009, I returned to the Lewes, Delaware branch of what was then Wachovia Bank. I

met with DuBreuil again and began the process of opening the first of three money

market accounts. I explained to him our goal of accumulating $1 million across four

accounts, staying within FDIC limits. Mr. DuBreuil seemed confused but opened the

account without further issue. When I mentioned that I would return the following

week to open another, he unexpectedly

reacted with hostility, snapping, "I'm not opening accounts all over the place just

for your fucking convenience."

This incident occurred after the previous interactions regarding the LLC/trust deposit,

which likely contributed to the tense atmosphere. From that point forward, I simply

conducted business using Wells Fargo accounts in Virginia and assumed I would never

deal with DuBreuil again. I may have mentioned DuBreuil's rudeness or

misunderstanding at the Virginia Wells Fargo - I don't recall, but I certainly didn't

advocate for his removal.

Signing of the MoU and Disbursement of $1,000,000 by DuBreuil

October 15, 2009 I needed all family members to sign and notarize the trust and Memorandum

of Understanding (MoU) documents. The family was located in Lewes, Delaware. I only needed a

notary, and we had used DuBreuil for that. I told Mr. DuBreuil very little about the trust or other

financial accounts or planning. I only mentioned that our family would be executing

a MoU transferring $1,000,000 to the boys, and that Bob, Jack,

and Mom would like him to review and comment on the trust documents. I simply needed the Trust

and MoU documents signed and notarized, and I thought Bob and Jack should at least hear a review

of the documents by someone other than myself.

Analyst Commentary: DuBreuil email saying he had reviewed the Trust/Mou."i spoke with your mom yesterday

and she seems to understand the trust"

Mom, Bob, Jack, and myself met with DuBreuil at Wachovia Bank in Lewes. The Trust Agreement,

LLC Operating Agreement, and MoU were reviewed, signed by family members, and notarized by DuBreuil.

DuBreuil's explanation of the trust was significantly incorrect, necessitating at least 12

corrections by me. The email stating he reviewed the documents, when compared to his actual

actions during the meeting, showed a clear lack of understanding. DuBreuil's demonstrably

inaccurate explanations of the trust raise serious concerns about his understanding or

competence in this area. His role was limited to notary.

DuBreuil then withdrew $1,000,000 from the 4 mm funds - closing the 3 unnecessary accounts,

and distributed the withdraw as per the MoU.

I again assumed I would never deal with Mr. DuBreuil again.

I provided Jack with a comprehensive account list including contact details. For the subsequent year, we

convened monthly to discuss Mom's estate, long-term care insurance, and the trust. It was apparent that

Jack had difficulty grasping these discussions, an observation outside my area of responsibility.

Mr. Masselli: Q Now, after Wells Fargo, where did you next work?

A

Swarthmore Financial Services, essentially it was a sub-agency of

Massachusetts Mutual Life Insurance Company

Q Now, when you were at Swarthmore, did you have any business relationship with Jack Beckett?

A Yes.

Q And what was that?

A Jack contacted me -- actually, Kristen contacted me and we discussed the situation with

Jack's -- you know, his management of Alberta's finances, and he was not able to get access to any of the records...he needed

to be able to access information regarding his mother's finances, and he could not; he told me he wasn't able to do that.

Q Are you referring to Kristen Long?

A Uh-huh. Yes, I am.

Analyst Commentary: (when did they meet) July 2010 thru February 2011

Q Thank you. Now, let's turn to, is it

Rockwell Associates?

A Uh-huh.

Q Where were they located?

A They were located in Wilmington, Delaware.

Q And how long have you worked there?

A From January of 2012 to the present.

Q And what are your responsibilities?

A I am essentially, I'm a financial adviser, so it is my responsibilities to prospect -- sales,

you know, prospect for clients.

Jack Given Management of Veazey Estate

I resigned as manager of the trust due to ongoing disagreements with Jack.

March 16 2011, Jack meets with attoney Thomas. Beckett notes:

No beneficiaires listed in trust (defective trust due to fact no beneficiaires list => refers to family)

* Left out what happens while trust is operating + when trust is terminated.

Poorly worded document!

"concocted Arrangements"

Mothers Estate is bizzare

Analyst Commentary: Who originated these trust takeaways?

March 21 2011, Kristen received and signed for box of financial documents. Jack in deposition speaks of shelf

of documents - he cataloged everything.

LyssaEast.com

Back to top of page

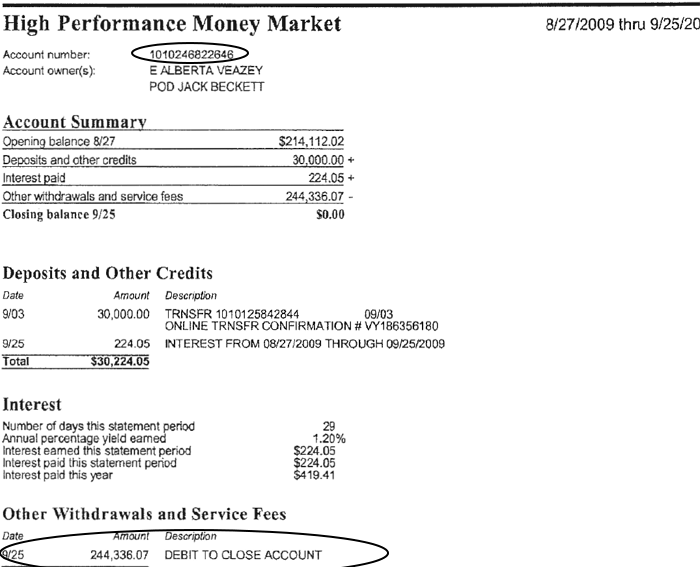

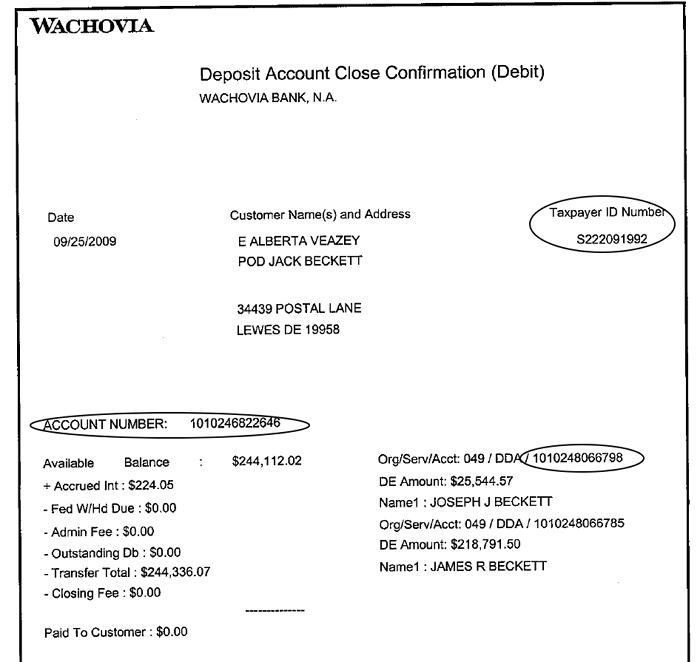

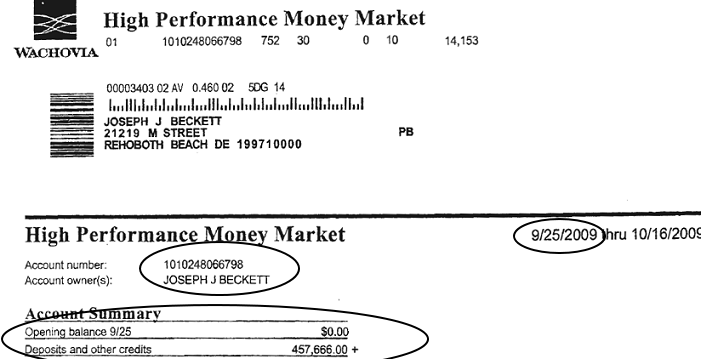

DuBreuil Fabricates [Account Zero]

Analyst Commentary: The "Fog of War" begins.

Analyst Commentary: In

deposition DuBreuil states how he explained the existence of [Account Zero]

to Jack, and his attorneys:

Q And could you tell me how it does that?

A If you look Alberta Veazey's share of Samuel Veazey's wrongful death lawsuit, that's part of

it. So I'm -- you know, if you look at that paragraph, on July 30th of `09, the sum, that sum was

deposited into equal shares, $427,833.32 [Account Zero] ... So those were deposited

into an account with her name on it.

DuBreuil's letter to the courts states:

"In order to fulfill his duties as Alberta’s guardian Jack made a number of attempts, through you, as the attoney for

Mrs. Veazey’s guardianship, to contact Jack’s brother, Donald B. (“Don”) Veazey, who had held Mrs. Veazey’s power

of attorney, in order to make an orderly transfer of legal title of Alberta Veazey’s assets

[Account Zero] over to the guardianship."

"There are indications that Don Veazey, who then was the managing member of the E. Alberta Veazey Family LLC,

transferred some, if not all, of the assets comprising Account #1 and Account #2 to Wachovia Bank

(Account #20000 3103

3332) (see Exhibit J) which is a checking account titled under the E. Alberta Veazey LLC.

This account appears to be used to pay various expenses of the LLC and maintain some asset liquidity."

Analyst Commentary: This one particular settlement disbursement, of 26 mesothelioma disbursements to Alberta, was $427,833.32.

The value of the LPL account was about $400,000, and the MoU gift amount was $418,000 to each.

So they must be the same thing.

Analyst Commentary: RIGHT?

Analyst Commentary: he then explains there were 4 mesothelioma disbursement of $427,833.32 pursuant to the MoU,

and is the funding for [Account Zero].

Analyst Commentary: so the DuBreuil logic flows: Alberta and Don received $418,000. And Alberta received $427,833.32

from the disbursement noted above, and it was put into qualified miller trust; The E. Alberta Family gifting trust.

Analyst Commentary: If we ignore the MoU's $1 million was funded from Alberta's accounts, DuBreuil could claim almost any amount

could be missing. DuBreuil claims "aggregate value of $842,000" in the DuBreuil/Karsnitz report for example.

Waiver of Notice

April 13, 2011 9:15 AM

Molina, Jessie

Subject: Alberta Veazey Petition/Joseph J. Beckett as Petitioner

Good Morning Mr. [Don] Veazey

Attached please find a Waiver of Notice

and Consent Delaware Chancery Court.

As your brother Jack might have communicated to you, it is

one of the

components of the petition Jack will be filing with Delaware Chancery Court to be appointed Mrs. Veazey's

guardian. Please fill it out, sign and notarize it, and return it to me at the address below.

Please note, I also sent this by letter yesterday.

If you have any questions, please do not hesitate to contact me at 302-856-3571.

Thank you very much for your help.

Jessie

Jessie O. Molina,

Legal Administrative Assistant to

Robert L. Thomas, Esquire

Young Conaway Stargatt & Taylor, LLP

110 W. Pine Street

P.O. Box 594

Georgetown, DE 19947

(302) 856-3571

(302) 856-9338 - Fax

jmolina@ycst.com

Seems like just a request for guardianship, OK I sign a Waiver of Notice and Consent from Delaware Chancery Court.

Friday, April 22, 2011 4:25 PM

From: DuBreuil

To:

RE: Well Fargo reports these [MM] accounts to have been closed as of that date.

Analyst Commentary: Above e-mail documents DuBreuil and his witch hunt.

May 25 2011 Sharp appointed Attorney Ad Litem.

June 2, 2011 Jack discussion with Sharp

Analyst Commentary: Did Jack tell Sharp about the monthly financial updates or box? This would be withholding evidence.

Analyst Commentary: Jack gave Sharp some financial info - didn't talk about MoU, and convinced Sharp money was missing per

DuBreuil.

June 3, 2011 "Later that day I [Sharp] spoke with Don about the Petition. He informed me that he supports the Petition."

June 6, 2011, "I [Sharp] spoke with Alberta's son Bob Beckett."

June 13, 2011 Jack transferred $1k from mom to LLC to "replenish" funds. Jack could have distributed funds to replenish

LLC checking from LLC investment account but would have had to talk to the LPL broker and was advised by DuBreuil not to contact LPL.

Jack/DuBreuil Access My Business Account

Analyst Commentary: DuBreuil states in e-mail to [?]: "Jack did mention something about a Wells Fargo account of Don's that was still bank-linked to one

Alberta's accounts that you felt should be de-linked. I [DuBreuil] am meeting with Jack on Monday at

Wells Fargo to try and take care of it."

June 21, 2011 Jack & DuBreuil went to the Wells Fargo bank, asked for and was given my wife's business account number by

Wells Fargo employee.

Focusing on the events of June 21, 2011: Mr. DuBreuil's email indicated he was meeting Jack at Wells Fargo to address

the linking between Don's and Alberta's accounts. However, on that very same day, Jack and Mr. DuBreuil obtained my wife's

business account number from a Wells Fargo employee.

Even if we only consider this single day, the fact that they obtained my wife's business account information on the same

day they were supposedly addressing a different account linkage raises serious questions about their purpose and the legality

of obtaining that specific account number. It suggests the acquisition of my wife's business account information was not a

part of the stated intention and could therefore be unauthorized and potentially illegal.

Analyst Commentary: It seems Sharp was furnished with a list of accounts by Jack. Ayvazian subsequently granted Jack

access to all accounts requested, without scrutinizing their ownership or the genuine necessity for access.

When searching for the allegedly stolen

$427,833.32 [Account Zero], Jack and DuBreuil using Jack's access, requested several years of my wife's

Wells Fargo accounts' register.

Obtaining someone's financial account information or access without proper authorization is illegal and carries

significant legal ramifications. The critical question here is: how was Ayvazian persuaded by Sharp that Jack warranted

access to my wife's account?

LyssaEast.com

Back to top of page

The Report of the Attorney Ad Litem June 21, 2011

MOORE & RUTT,P.A.

James P. Sharp, Esquire

Attorney Ad Litem

122 West Market Street

P. O. Box 554

Georgetown, DE 19947

IN THE COURT OF CHANCERY OF THE STATE OF DELAWARE C.M. No. 15916-S

I evaluate and question the report's opening premises:

Sharp took my statement regarding mom's finances while I was touring Alcatraz in San Francisco.

Sharp struggled with my explanation of an irrevocable trust.

Sharp States:

According to Don, he consulted with a Virginia attorney named John Ryan to create a

Trust and Limited Liability Company on his mother's behalf.

He explained to me that the settlement proceeds were put into the Trust for Alberta's benefit. When she passes away,

the remaining assets will go to her children.

DuBreuil originated this explanation a year prior and is a fabrication that does not reflect my communication with Sharp.

I unequivocally explained that the trust was an irrevocable Medicaid Trust funded with a $285,000 gifted to the trust June 2009.

I never made this statement alleged by Sharp and this statement contaminates Sharp's entire presentation to the court.

Sharp notes discussions with Thomas (who was himself in discussions with Ryan), yet no mention is made of this vital context.

This suggests a significant breakdown in the relay of accurate information, either from Thomas to Sharp, or in Sharp's subsequent

reporting.

Sharp seems to have called Ryan while Ryan was on vacation.

Sharp States:

Sharp: "Jack has some questions about the establishment of the Trust"

Analyst Commentary: October 15, 2009, Jack personally participated and witnessed DuBreuil review the Trust and LLC

Operating Agreement with the family and Jack signed those documents.

Sharp States:

When I spoke with Don, I specifically asked him about his mother's finances ... Don

advised me that the Trust consisted of the following:

1) the house at Postal Lane,

2) a money market account with approximately $10,000.00,

3) a checking account with approximately $6,000.00, and

4) a stock brokerage account with approximately $19,000.00.

The following constitutes the correct, accurate, and precise detail of Trust and Estate assets as of March 1, 2011. This excerpt

is derived from documentation provided by Jack in accordance with discovery in the Virginia litigation, which documentation

was under Jack's control as of the date of this report:

A correct list of the LLC's [trust] assets June 1, 2011:

1) the house at Postal Lane,

2) a money market account [Wells Fargo 20000 3103 3345] with approximately $10,000.00

3) a checking account [Wells Fargo 20000 3103 3332] with approximately $6,000.00

Analyst Commentary: The two above accounts are those DuBreuil believes all lawsuit proceeds

should be deposited to.

4) a stock brokerage account [LPL 5451-7282] with approximately

$400,000.00

5) a Nationwide annuity [01-6049490] with approximately

$200,000.00

A correct list of Alberta's [estate] assets June 1, 2011:

1) a car $13,000

2) a truck $3,000

3) a stock brokerage account with approximately $19,000.00 including 200 shares of Lowe's

stock valued at approximately $4,000.00

4) a safety deposit box with gold valued at $30,000.00, silver service set valued at $6,000.00, and

four coins valued at $2,400.00

5) bob's debt $40,000

6) Wells Fargo checking

7) Well Fargo money market

Analyst Commentary: total estate assets June 2011:

$113,400.00

Ryan email to Thomas re: above

Analyst Commentary: The preceding section was a static snapshot June 1, 2011.

Analyst Commentary: Sharp now begins a Time period money flow analysis December 2008 through June 2011:

Sharp States:

Even though Alberta received a great deal of money from the aforementioned settlement, it is unclear

where that money went.

It was unclear what happened to the settlement proceeds she received from the

mesothelioma suit.

A correct and generalized money flow analysis:

1) proceeds from closing Alberta's investment accounts $100,000+.

2) proceeds from mesothelioma litigation $1,300,000+

3) outlay gift via MoU $1,000,000

4) outlay gifting to boys Jan - Dec 2010 $45,000

5) outlay gifting to establish of the Trust $285,000

6) outlay purchase car $13,000

7) outlay home care

8) outlay personal expenses

Sharp States:

Don admitted to me that he started the process to receive these payments but did not follow through on

completing it. Only recently has Jack stepped in to correspond with the insurance company.

1) Only Jack, with POA health could apply. I submitted the application and only needed Jack to submit

his POA health documents to insurance.

2) DuBreuil told Jack she had plenty of money and didn't need long term care insurance payment.

3) Jack's attorney sent me a email saying Jack didn't want to be micromanaged by me.

Sharp States:

I was disappointed to hear that he [Don] failed to adequately handle his mother's bills since

she was moved to Brandywine.

False statement. I handled all her bills and all were paid on time & there was an estate plan.

Long term care plan

Cost:

Brandywine $6,000 /month increasing to $8,000 /month - using

an average of $7,000/month

Source of funds:

Social Security $2,000

Long term care $3,000

Cash and Assets on hand: $113,400/60 months =

$2,000+-

This simple back of the napkin, single page analysis I give here should be kept in mind when

reviewing the Sharp report and the DuBreuil financial analysis below.

I evaluate and refute the 10 paragraphs listed under Alberta's Assets and Finances:

I have reason to believe paragraphs 1, 2, and 3 of this section was written by Bob Beckett. Bob attended night law school.

He tried numerous times to pass the bar but was unable. Bob worked as a receptionist at a dental office. Bob would

have gotten all info from Jack or DuBreuil.

These paragraphs raise concerns about the writer's attention to detail

and clarity. It does not necessarily prove that the writer is inexperienced, but it suggests that

the writing could be significantly improved. The lack of detail, and passive voice used,

are things that an experienced attorney would typically avoid. Based on these observations, it's

reasonable to conclude that the writer's legal experience is likely limited or that they are not

paying close enough attention to the details of their work.

Bob struggled with writing; said he wanted to work with Trusts and Estates.

Refutation of Paragraph 1:

Sharp States:

"During my investigation, i discussed with Don, Jack, and Bob my concerns about

Alberta’s assets. According to Jack, Alberta owns her home free and clear

of all mortgages, liens, etc. it is believed that she also has ample liquid resources available

for her care from a settlement related to Sam Veazey’s death. Evidently, Sam suffered from

medical problems related to mesothelioma. the Veazeys filed a lawsuit and

received a hefty settlement. Because Sam was Don's father, Don was involved in the

lawsuit. Jack and Bob, however, were not involved in the suit even though Sam was

very close to them because they were Sam’s stepsons. Jack advised me that the settlement

proceeds were split four ways with Don, Jack, Bob, and Alberta each receiving over $400,000

Alberta received 3/4 of the settlement and distributed shares to Jack and Bob"

The initial paragraph's analysis of Alberta's assets is fundamentally flawed, relying on

incomplete and potentially biased information. Key inaccuracies include:

Incomplete Asset Discussion:

The investigator's discussion of assets with Don, Jack, and Bob is presented as comprehensive,

but this is misleading. Thomas was also involved in asset discussions, and this omission

creates an incomplete and inaccurate narrative.

False Claim of Unencumbered Home Ownership:

Jack's assertion that Alberta owns her home "free and clear" is demonstrably false. The

property is held within a trust, a critical detail that significantly alters the

understanding of her asset ownership.

Misrepresentation of Asset Sources:

The statement that Alberta's "ample liquid assets" derive solely from the Sam Veazey

settlement is incomplete. Her assets originate from diverse sources, and this narrow

focus misrepresents her true financial situation.

Incorrect Family Relationships and Settlement Participation:

The claim that Sam Veazey was Jack and Bob's stepfather and that they participated in

the mesothelioma settlement is incorrect. Jack and Bob were never legally adopted and,

therefore, had no legal claim to the settlement (standing). Bob penned several e-mails

indicating he did have "Standing".

Contradictory and Oversimplified Settlement Distribution:

Jack's description of the settlement being split "four ways" and then Alberta receiving

"3/4" is both contradictory and an oversimplification. A more accurate and concise description

is provided in my synopsis above.

Jack's Unreliability and Bias:

Jack's refusal to review relevant documents suggests a lack of thoroughness or a deliberate

attempt to maintain a skewed narrative. His repeated expressions of dissatisfaction with his

perceived share of the settlement, coupled with accusations of stolen money, reveal a clear

bias. Furthermore, his statement that it is believed that she has ample liquid resources, is

based on his misunderstanding, and disregards the actual financial plan.

Internal Contradictions:

The paragraph contains internal contradictions regarding the settlement distribution.

First it states that the settlement was split four ways, then it states Alberta received

3/4. These two statements are not compatible.

Vague and Misleading Terminology:

The term "ample liquid resources" is vague, and based on Jacks misunderstanding, and

disregards the actual financial plan.

These inaccuracies and inconsistencies demonstrate the unreliability of the paragraph's

analysis and necessitate significant correction.

Refutation of Paragraph 2:

Sharp States:

"Even though Alberta received a great deal of money from the aforementioned

settlement, it is unclear where that money went. According to Don, he consulted with

Virginia attorney Named John Ryan to create a trust and LLC on his mother's behalf. He explained

to me that the settlement proceeds were put into the trust for Alberta’s benefit. when she

passes away, the remaining assets will go to her children."

Misrepresentation of Fund Placement:

The statement that "the settlement proceeds were put into the trust" is false.

No settlement funds were placed into the existing trust. Instead, the majority of those funds were

gifted to Jack and Bob.

Nature of the Existing Trust:

The existing trust is a Medicaid trust. It is specifically designed for Medicaid eligibility

purposes and does not provide for Alberta's direct benefit or use of funds. This is a critical

distinction that the paragraph fails to acknowledge.

Refutation of "For Alberta's Benefit":

The paragraph's assertion that the funds were placed in a trust "for Alberta's benefit" is

incorrect in regards to the existing trust. The funds were gifted, and the existing trust is a

Medicaid trust, not a vehicle for her direct financial benefit. This seems to echo DuBreuil's

explanation of the estate. The investigator speaks of "a Virginia attorney named John Ryan" but

seems to not have talked to him.

The investigator's statement

"He explained to me that the settlement proceeds were put into

the trust for Alberta’s benefit. When she passes away, the remaining assets will go to her

children. "Echoing DuBreuil's erroneous explanation and may be the "he" referred to here.

This repetition of inaccurate information further undermines the investigator's credibility

and highlights the flawed nature of their analysis.

Refutation of Paragraph 3:

Sharp States:

"Mr. Thomas provided a copy of the Trust and Limited Liability Agreement for my review. The

documents were prepared under Virginia law and were executed on June

18, 2009. The Trust names Don as the Trustee and Jack as the back-up trustee. Article l }

Paragraph 1(1) of the Trust identifies Don, Jack, and Bob as the beneficiaries and

distributions may be made to benefit them. The main asset in the Trust was a 100%

interest in the LLC. The main asset of the LLC was Alberta's interest in her home

in Sussex County, Delaware (presumably her residence on Postal Lane), What has troubled

me about the Trust is that there is no provision that the assets be used for

Alberta's benefit, It appears as though she created the Trust so that she could pass

the assets to her children while she was alive. I also note that the Trust is irrevocable.

A copy of the Trust is attached hereto as Exhibit A, Likewise, the LLC C)operating

Agreement appears to be designed for the benefit of Alberta's children and not Alberta.

The only members of the LLC are Don and the Trust. 4 A copy of the LLC C)operating

agreement is attached hereto as Exhibit B. On September 28 2009, Alberta transferred

her property located at 34439 Postal Lane in Lewes to the LLC via deed. This deed was

also prepared by Virginia counsel. A copy of the deed is attached hereto as Exhibit C."

Paragraph 3 presents a superficial analysis of the Trust and LLC documents,

failing to grasp the fundamental purpose of these instruments within the context

of Medicaid planning.

Medicaid Trust Context:

The investigator's concern regarding the absence of provisions for Alberta's direct benefit

reveals a critical misunderstanding. The Trust in question is a Medicaid trust, specifically

structured to protect assets for Medicaid eligibility. Its primary objective is not to provide

direct distributions to Alberta, but to preserve assets while adhering to Medicaid regulations.

This is a standard and legally sound estate planning strategy in elder law.

Irrevocability and Asset Protection:

The irrevocable nature of the Trust, noted by the investigator, is a necessary component

of Medicaid planning. This feature prevents assets from being counted towards Alberta's

eligibility threshold, ensuring her access to essential long-term care services.

Beneficiary Designation and Asset Preservation:

The designation of Don, Jack, and Bob as beneficiaries is consistent with the Trust's purpose.

This structure allows for the eventual transfer of assets while safeguarding them from Medicaid

spend-down requirements.

LLC's Role in Asset Management:

The LLC serves as a vehicle for asset management and protection. Its primary assets are Alberta's

residence and, importantly, an investment fund. These are common tools used in conjunction with

Medicaid trusts to further shield assets.

Misinterpretation of Intent:

The investigator's speculation that Alberta created the Trust to "pass assets to her children

while she was alive" is a simplistic and inaccurate interpretation. Here, I believe the investigator

is confusing the MoU with the trust. The Trust's creation was

motivated by the need for Medicaid planning, a complex legal strategy, not merely a desire for

premature asset transfer.

Omission of Key Asset:

The investigator states that the main asset of the LLC was Alberta's interest in her home. This

is incomplete. The main asset of the LLC was an investment fund, followed by Alberta's interest

in her home. This omission shows a lack of due diligence.

Investigator's Lack of Due Diligence:

The investigator's analysis is flawed by the omission of the Medicaid context. The investigator

also failed to speak to the attorney that created the documents.

Refutation of Paragraph 4:

Sharp States:

"When I spoke with Don, I specifically asked him about his mother's finances, which he

controlled (as acknowledged by all family members including Alberta). Don advised me

that the Trust consisted of the following: 1) the house at Postal Lane, 2) a money market

account with approximately $10,000.00, 3) a checking account with approximately $6,000.00,

and 4) a stock brokerage account with approximately $19,000.00. Alberta also owns a car, a

truck, and 200 shares of Lowe's stock valued at approximately $4,000.00. Don also believes

that Alberta has a safety deposit box with gold valued at $30,000.00, silver service set

valued at $6,000.00, and four coins valued at $2,400.00. It was unclear what happened to

the settlement proceeds she received from the mesothelioma suit."

This paragraph demonstrates a fundamental misunderstanding of the separation between

the gifted (MoU) funds, the assets held within the established Medicaid trust,

and the assets remaining within Alberta's personal estate. The settlement funds were

gifted to Jack and Bob, and are no longer a part of Alberta's estate. The trust assets

are for Medicaid planning, and separate from Alberta's personal holdings. The reporting

of these amounts without proper context creates a misleading picture of Alberta's financial

situation. It's worth noting this same confusion is echoed by DuBreuil in his March 21, 2012

letter to the courts, Paragraph 5; Subsection 6: "Alberta Veazey’s share of Samuel Veazey’s

Wrongful Death Lawsuit".

It is crucial to differentiate between these distinct categories of assets to provide

an accurate and comprehensive understanding of Alberta's financial landscape. Therefore, while

the paragraph may contain some factual information, the lack of contextual understanding

regarding the gifting of funds, and the separation of the trust and estate, renders the

analysis incomplete and misleading.

Refutation of Paragraph 5/6:

Sharp States:

"The issue about locating Alberta's finances has been further complicated by Don's recent

abdication of his responsibilities as Trustee, Power-of-Attorney, and Manager of the LLC.

In April 2011 1 Mr. Ryan sent a letter to Jack on Don's behalf advising Jack of Don's

resignation. A copy of this letter is attached hereto as Exhibit D. When I spoke with Don,

he admitted that he had been "overwhelmed" and was quite nervous about these issues,

He also did not appear to have a solid comprehension of the specifics of the Trust and

LLC agreement; something found surprising since he was the person who evidently arranged

for the consultation with Mr. Ryan."

locating Alberta's finances has been further complicated...:

The investigator fails to define how so.

Resignation, Not Abdication:

The term "abdication" is inaccurate. I resigned from my positions as Trustee, Power-of-Attorney,

and LLC Manager. This was a considered decision, not an abandonment of responsibility.

Context of Resignation: Jack and DuBreuil's Influence:

My resignation was primarily driven by Jack's insistent demands for DuBreuil to manage

Alberta's affairs. This, coupled with the misinformation DuBreuil was disseminating,

created an untenable situation.

Frustration, Not Overwhelm or Nervousness:

The investigator's portrayal of me as "overwhelmed" and "nervous" is inaccurate.

I was not but rather frustrated at Jack's relentless push for DuBreuil's involvement and

by the deliberate misinformation DuBreuil was providing, which threatened to undermine

the carefully planned Medicaid protection strategies.

Demonstrated Understanding:

My involvement in establishing the Trust and LLC, and my ongoing awareness of their purpose

within the Medicaid planning context, demonstrates my understanding of the relevant aspects.

I fully understood the documents, and their purpose.

Consultation with Attorney Ryan:

Arranging the consultation with Attorney Ryan was a responsible step in ensuring proper

asset protection for Medicaid eligibility. I understood the overall plan.

Omission of Medicaid Context:

The investigator continues to omit the most important factor, the trust is a Medicaid trust.

This omission taints the investigator's entire analysis.

DuBreuil's Misinformation:

The investigators report fails to mention the misinformation that DuBreuil was providing,

which was a large factor in my frustration.

By providing these clarifications, I address the mischaracterizations, reveal the influence

of Jack and, by proxy, DuBreuil, and provide a more accurate and complete picture of my

actions and understanding.

Refutation of Paragraph 7: Alberta's ability to pay for care:

Sharp States:

"While I was surprised to hear that Don did not have a good understanding about the Trust

and the LLC, I was disappointed to hear that he failed to adequately handle his mother's

bills since she was moved to Brandywine. Evidently, Alberta has a long-term care insurance

policy that will pay up to $72,000.00 in costs associated with residence in a long-term care

facility such as Brandywine. My understanding is that the policy will pay approximately $3,000.00

per month. Don admitted to me that he started the process to receive these payments but did not

follow through on completing it. Only recently has Jack stepped in to correspond with the

insurance company. In the meantime, Jack has been paying out of his own funds the bills

associated with Alberta's stay at Brandywine. It is my understanding that Alberta receives

approximately $2,000 per month from Social Security. Brandywine costs approximately $6,000.00 per

month so the insurance policy, if used, would greatly reduce the need to dip into Alberta's

liquid assets."

"failed to adequately handle his mother's bills"

The assertion that I "failed to adequately handle" Alberta's bills is a gross mischaracterization.

There is no proof of this offered at any time during litigation or otherwise. Blatant lie.

Jack's Exclusive POA Health and Refusal:

Jack held the exclusive Power of Attorney for health, granting him sole authority to apply for the

long-term care insurance. He refused to do so, citing his dislike of being "micromanaged by

me. He will get to it when he has time." This refusal directly impeded the timely processing

of the insurance claim.

Jack's Refusal to Act:

The delay in finalizing the long-term care insurance process was solely due to Jack's refusal

to file the claim. I was unable to act due to the limitations of my Power of Attorney. While

Jack's eventual involvement in corresponding with the insurance company is noted, it is

essential to emphasize that he intentionally delayed the process by refusing to file the

claim.

Medicaid Planning Context:

The high cost of Brandywine is a significant factor. The investigator continues to ignore the overarching strategy of Medicaid planning. The protection of Alberta's liquid assets is a deliberate and necessary step to ensure her long-term care needs are met without jeopardizing her eligibility for benefits.

Misrepresentation of Responsibility:

The investigator's report implies that I was responsible for the insurance claim, when in fact,

Jack was the only person with the legal ability to file the claim.

These clarifications expose the misrepresentation of responsibility and offer a

more accurate representation of the situation. Note the insurance would pay $3,000 per

month for 3 of the Medicaid look back of 5 years.

Refutation of Paragraph 8: Bob's debt:

Sharp States:

"There is also a question as to whether Bob owes his mother money for an outstanding debt.

Mr. Ryan references this debt in his letter. I sense that there is some dispute as to whether

a debt is actually owed and, if so, how much is owed. Nonetheless, I believe that the guardian,

if appointed, should investigate this matter as well."

Bob frequently "borrowed" money from Alberta over the years. This was a recurring pattern.

Jack often spoke of bob's debt being $40,000. It is important to acknowledge that Bob did

receive a substantial gift of $457,666.

When planning Alberta's care and estate, I factored in the potential debt owed by Bob. This

was a consideration in the overall financial planning.

Refutation of Paragraph 9: Discuss these concerns with Alberta:

Sharp States:

"I explained to her that Jack had been paying her bills of late with his own money"

Did you tell my mother, who has Alzheimer's and is in a care home, that she was out of

money and couldn't pay her bills?

Oh ... My ... God.

Refutation of Paragraph 10: equitable relief may be necessary:

Sharp States:

"Ultimately, I think that whoever is appointed guardian of Alberta's property should make a

thorough investigation about Alberta's finances and assets. The potential lack of assets

available to pay for Alberta's care concerns me. If the guardian is unable to find out

adequate information from this investigation, it is quite possible that an action for an

accounting and other equitable relief may be necessary."

This is where he makes a case for account access. Just so happens to have a list of

accounts. Including my

wife's business account.

The court was presented with information that was a stunningly blatant misrepresentation of

the facts. The attorney must take particular care in weighing the strengths and weaknesses

of the evidence if there are grave consequences for those involved.

Analyst Commentary: Misrepresentation in court can have severe consequences, including sanctions, penalties,

and criminal charges.

A recently licensed attorney, should understand irrevocable trusts, especially if they have

focused their studies or early practice in areas like:

- Estate Planning: Irrevocable trusts are a fundamental tool in estate planning. Trust and Estate Law: This area of law specifically deals with the creation, administration, and distribution of trusts and estates.

- Elder Law: Irrevocable trusts are often used in elder law to protect assets for Medicaid eligibility.

- Tax Law: Irrevocable trusts have significant tax implications, and attorneys specializing in tax law should be familiar with them.

- Law School Curriculum: Most law schools cover the basics of trust law, including the distinction between revocable and irrevocable trusts.

- Bar Exam: Bar exams often include questions on trust law, requiring candidates to demonstrate their understanding of irrevocable trusts.

Bob's involvement as "an attorney in San Francisco" gave credibility to the Sharp report.

Analyst Commentary: transcripts needed.

June 24, 2011 Jack appointed guardian

June 27, 2011

From: Thomas

To: John Ryan

RE: documentation/lnfomation requested of your client, Donald Veazey

e-mail is alleged by Thomas

July 13, 2011

From: Thomas

To: John Ryan

RE: Reply status inquiry

We are trying to finalize the Inventory required by the Court in the context of the Alberta Veazey guardianship proceedings; and, toward that end, I await the documentation/lnfomation requested of your client, Donald Veazey, in connection with his capacities as, rspectlvefy, manager of E. Alberta Veazey Family LLC and trustee of the E. Alberta Veazey Family Gifting Trust.

Thursday, July 14, 2011

From: John Ryan

To: Don

I was contacted by Robert Thomas - the attorney who handled the guardianship Petition for your brother. They are requesting that you provide an accounting for the LLC and the Trust from inception in 2009 to the date when you last took action on behalf of the entities.

Thursday, July 14, 2011 5:31 PM

From: Thomas, Robert

To: John Ryan

Subject: RE: Veazey - E. Alberta Veazey/Joseph J. Beckett Guardian - My letter dated June 27, 2011 - Reply status inquiry

Thanks for your reply (and I did receive from your assistant a pdf of the signed LLC agreement)

Analyst Commentary: Jack has been given and aparently lost his copy from the October 15, 2009 MoU signing, the copy provided to him (signed for March 21, 2011), or the copy I made and mailed to him April 2011.

Friday, July 22, 2011 10:29 AM

From: John Ryan

To: Thomas, Robert

subject: Re: Veazey - E. Alberta Veazey/Joseph J. Beckett Guardian - Status update inquiry

Bob:

Don was out of town on an extended trip and just returned my calls/emails yesterday ...

Analyst Commentary: July 22, 2011 "next court date" so they go to court not understanding the trust.

July 22, 2011

From: Thomas

To: Ryan

RE: were gift tax returns for transfer of house, nationwide filed? [my understanding it wasn't necessary]

July 22, 2011 2:29:41 P.M.

From: Thomas

To: Ryan

Re: Veazey - E. Alberta Veazey/Joseph J. Beckett Guardian - Status update inquiry

Thanks for your reply. Needless to say, the information which you provided is a ton more than I had prior to receipt of your

email. On the strength of your email, we will file the Inventory on the basis that neither the LLC nor Trust are part of Mrs

Veazey's guardianship estate.

*** Massachusetts Mutual Life Insurance Company / Penn Mutual Life Insurance Company/HTK (Hornor, Townsend & Kent, LLC) / & DuBreuil's attack begins here ***

Analyst Commentary: November 30 Pep Talk - you have one more month to produce or your...Wednesday, November 30, 2011 4:25 PM

From: DuBreuil

To: Thomas

RE: Veazey – E Alberta Veazey

Bob [Thomas],

I have a legal question related to the Alberta Veazey...Now that Jack Beckett is Mrs. Veazey's legal guardian, and is

required to provide for her financially, does Jacks guardianship role supersede Don's role as POA. In other words could

Jack have the legal right to manage these accounts as he saw fit to provide for his mother's care without having to go through Don?

Wednesday, November 30, 2011 5:09 PM

From: Thomas

To: DuBreuil

RE: Veazey – E Alberta Veazey – Question from Tom DuBreuil RE POA Titled Assets

Tom [DuBreuil],

My sense, without research, is that Jack's guardianship appointment trumps Don's power of attorney and that Jack now

is positioned to revoke any power of attorney granted by his mother. Once we have a good understanding of the

accounts/policies/etc. of Mrs. Veazey still in play but currently not titled in the name of the guardianship, we can pursue getting

those assets retitled into the name of the guardianship.

Wednesday, November 30, 2011 7:35 PM

From: DuBreuil

To: Thomas

RE: Veazey – E Alberta Veazey – Question from Tom DuBreuil RE POA Titled Assets

Bob [Thomas],

That is what I thought I will send you what documentation that I have about the accounts

before I have the financial planning software populated with all of the data. I will call Jack to

see if he has a copy of the POA for you to research.

Thursday, December 1, 2011

From: DuBreuil

To: Jack Beckett

Mesothelioma Settlement

Jack & Kristin, Do either of you remember or have a record of what the total settlement from Sam Veazey's wrongful death law suit was.

Thursday, December 1, 2011

From: DuBreuil

To: Bob Thomas

FW: RE: Veazey – E Alberta Veazey – Question from Tom DuBreuil RE POA Titled Assets

[Bob,] ...would you be able to determine if Jack's guardianship agreement would be able to supersede Don's POA

From: Thomas

To: DuBreuil

[Tom,] ...Jack's guardian capacity allows him to revoke the POA; and I intend to have him do that once we have a handle on the accounts which are titled in the name of the POA or which we otherwise learn are tied in some fashion to the POA.

Thursday, December 1, 2011

From: DuBreuil

To: Thomas

E. Alberta Veazey POA Accounts

...Don somehow managed to name himself as the annuitant [Nationwide Annuity].

Monday, December 5, 2011

From: DuBreuil

To: Thomas

RE: Veazey – E. Alberta Veazey – Email of 12/1/11 from Don Beckett to Jack Beckett RE: Need to Withdraw from Nationwide Annuity

Don suggested a withdraw from the Annuity preparing the trust for taxes for 2012

[DuBreuil to Thomas] Why does the Family LLC need to withdraw money from Alberta's personal money [Nationwide Annuity] for taxes

Monday, December 5, 2011

From: DuBreuil

To: Jack

RE: Veazey – E. Alberta Veazey – Email of 12/1/11 from Don Beckett to Jack Beckett RE: Need to Withdraw from Nationwide Annuity

DuBreuil begins his "research" here, eventually fabricating [Account Zero]

Also, I came across 2 Wachovia money market statements that were opened for Alberta on

7/30/09 (see attachments). They are the first statements issued for these accounts. Note

two identical deposits for $213,916.66 made in each account, and the account titling E.

Alberta Veazey POD Bob Beckett and Jack Beckett. The accounts may represent Alberta's

share of Sam's wrongful death settlement. Can you find and send me any and all statements

you have for these specific accounts?

As a matter of fact any bank statements of Alberta's, Wachovia or otherwise, that you can

come up with and get to me from June 2009 to the present would be helpful. This may be

the best way to track the money trail.

Analyst Commentary: ... and 2 x $213,916.66 is $427,833.32, the source of funds for [Account Zero]

Thursday, December 15, 2011

From: DuBreuil

To: Thomas

RE: Veazey – Don's 12/12/11 email captioned “LLC year-end tax planning”

DuBreuil strongly disagrees with my attorney Ryan as to the ownership of the Annuity

...he [Don] indicated that the "Nationwide Annuity", contract# 01-6049490, was an asset of the gifting trust...quarterly statement of the Nationwide Annuity, Apr 1 2011 to June 30,2011 is not titled as an asset of the trust. It is titled Donald B Veazey, POA-Donald B Veazey, Donald Veazey-Annuitant.

Monday, December 19, 2011

From: DuBreuil

To: Jack

FW: Veazey – Don's 12/12/11 email captioned “LLC year-end tax planning”

...legal titling on the Nationwide Annuity does not indicate that it is part of the Veazey Family LLC through the gifting trust

Analyst Commentary: Monday, December 19, 2011 Jack & Kristen meet DuBreuil at Swarthmore

Tuesday, December 20, 2011

From: DuBreuil

To: Thomas

...me to formally deliver to Jack Alberta Veazey's financial plan that I have been working on, along with my suggestion on how to ensure that there is an income stream to pay for Alberta's nursing home care.

Analyst Commentary:

Did DuBreuil know he was moving to Rockwell Associates in 3 weeks? Would this not be something

to propose after starting the new job?

LyssaEast.com

Back to top of page

Thomas, Karsnitz, DuBreuil & Rockwell Associates' Accusations and The Fog of War

Analyst Commentary: Jack's deposition speaks of "they all" got together.

maybe compiled the DuBreuil document together.

Analyst Commentary: December 2011, Debreuil, Kristen, Jack, and Thomas discussed the details of a

document Karsnitz would need to present to Sam Glasscock and the Delaware courts to bring civil and criminal

charges against me.

From: DuBreuil

To: Jack

Dear Jack,

This e-mail ls to confirm our scheduled meeting on Jan 31 at my new office @ 3:30pm

Jacks states he will bring criminal charges after the holidays document

According to an email by Mr. Masselli "Jack really didn't

have a clue about the many EAV and LLC accounts [the trust vs estate]. Jack and Bob Thomas

turned to DuBreuil ... Furthermore, he [DuBreuil] doesn't seem to have a great memory of what

went on when he was at Wachovia."

- DuBreuil - DEPOSED TWICE

- Jack - DEPOSED TWICE

- Kristen - DEPOSED

- Thomas - REFUSED TO BE DEPOSED

- Karsnitz - ATTORNEY/CLIENT

- Warrenton -

- Sharp - REFUSED TO BE DEPOSED

DuBreuil Begins Rockwell Associates Monday, January 9, 2012

From: DuBreuil

To: Thomas

New Contact info

DuBreuil agrees to hold off bringing litigation against Don.

Bob, thanks for the call today. I will review what you send me, then explain it to Jack. What you described sounds like a better way to go as opposed to litigation.

From: DuBreuil

To: Jack

DuBreuil further insert himself.

I have had several conversations with Bob Thomas today and we seem to have some

direction on how to handle Alberta's money issues.

...Alberta's personal assets where Don is POA Bob [Thomas] feels that your

guardianship agreement supersedes Don's POA. Getting those assets under your

control may be nothing more than a phone call to the appropriate companies...

Monday, January 23,2012

From: Thomas

To: DuBreuil

Veazey - E. Alberta Veazey • LLC Action of Sole Member Appointing Jack as Successor Manager

As l indicated when you and I spoke, having determined a while back that Donald was not going to cooperate, I prepared the attached action so that Jack, unilaterally, could replace Don.

Tuesday, January 24, 2012

From: DuBreuil

To: Thomas

... attachment is the confirmation letter now listing Jack Beckett as Alberta's Guardian on her Nationwide Annuity account. This means Jack can officially conduct business on this account.

February 8, 2012

From: DuBreuil

To: Thomas

Bob,

See attached copy of letter of instruction sent to Nationwide Annuity Co. to transfer annuity to Jack Beckett's guardianship

February 20, 2012

From: DuBreuil

To: Thomas

As of right now I have run into a dead end as to where the lawsuit money or the brokerage account money went. I calculate that about $275,000 of Alberta's money is unaccounted for.

Analyst Commentary: DuBreuil has found more money stolen.

MR. MASSELLI: ... reaction from either Jack or Thomas to your statement that you couldn't account for $275,000?

...so I don't remember if Bob gave a reaction, and I don't remember what Jack had said

Consequences of DuBreuil being wrong

MS. MURPHY: Objection, speculative. He can answer, if he has the information.

MR. MASSELLI: Let me be very clear about this, because I want this on the record.

Mr. DuBreuil,

who is a qualified financial analyst with a long career, in this Email and several subsequent documents that

we will be considering is making estimates of essentially

whether money is missing or money isn't missing;

MR. MASSELLI: ... what Mr. DuBreuil had before him, especially because, unfortunately,

in discovery, we were not provided with some documents that are -- not by

him, but documents that he says in various Emails that he gave to Mr. Beckett or gave to Mr. Thomas and, because

of that, I'm just trying to get a feel for what the basis of certain statements was and wasn't.

MR. MASSELLI: ... putting a 91-page document into the transcript

Q Okay, I'd like to show you an exhibit that I'm going to mark as

Exhibit 31, which is a document that you sent to me

last week, which appears to be a

letter dated March 1st, 2012 to Robert Thomas.

A That's right.

Q I'll give you that copy as well so you can keep it.

A That would be part of the exhibit, all right.

Q Yes.

A I'll go off of that, okay.

(DuBreuil Exhibit 31, marked for identification.)

Thursday, March 1, 2012 to Robert Thomas

From: Thomas To: DuBreuil Re: Part of the answer to "where has the money gone" may be answered by the gift tax returns which John Ryan reported that he had filed pertinent to transfers by Mrs. Veazey when the LLC and trust were set up .

Analyst Commentary: Did Karsnitz know of Ryan/Thomas conversation?

LyssaEast.com

Back to top of page

Analyst Commentary: DuBreuil did not wait for updates from the attorneys sending his official e-mail:

From: DuBreuil

To: Thomas

RE: Veazey - E. Alberta Veazey - Tom DuBreuil Analysis of EAV Financial Account

Bob,

This is also being shared with Craig Karsnitz.

The document titled "Tom DuBruell Analysis of EAV Financial Account" is a 91-page instrument containing false accusations

of theft against me concerning my parents' estate. This fraudulent document was submitted as evidence March 21, 2012 in the

Delaware courts, directly leading to a wrongful lawsuit initiated against me in Virginia. As a direct consequence, I have

suffered substantial damages, including significant reputational harm, emotional stress and hundreds of thousands of dollars

in legal fees and financial losses.

Critically, this document omits a $1 million gift that DuBreuil himself withdrew October 15, 2009 and distributed pursuant to

a notarized agreement (Memorandum of Understanding). This omission is not a mere error; it constitutes a deliberate

misrepresentation of fact indicative of DuBreuil's deceptive tactics and the manipulated nature of the document.

The Rockwell Associates/DuBreuil/Karsnitz document unequivocally accuses me of theft and was fabricated with the intent

to prejudice the court's opinion regarding my administration of my parents' estate.

A Trial Is Held

March 2012 Karsnitz/Thomas presented the Rockwell/DuBreuil "E. Alberta Veazey Analysis of Financial Transactions"

document to Glasscock.

Analyst Commentary: It appears Mr. DuBreuil holds a misconception regarding the mesothelioma litigation, seemingly

conflating it with the 'E. Alberta Veazey Family LLC.

Analyst Commentary: email June 24, 2009 Re: deposit

2) deposition quote: proceeds from the mesothelioma lawsuit were going to be placed in the LLC.

DuBreuil's statements, summarized from DuBreuil first deposition, pages 51 through 66, on this matter include:

- "I did not discuss the mesothelioma litigation with Alberta."

- "Don [Veazey] handled the mesothelioma litigation."

- "I became aware that a limited liability company existed."

- "I didn't really have an understanding ... what the limited liability company was going to be."

- "I don't remember discussing that the limited liability company existed and the purpose of it."

- "I opened 200003103 3345 E. Alberta Veazey Family LLC savings."

- "I opened 200003103 3332 E. Alberta Veazey Family LLC checking."

- Regarding understanding the reason for the gifting trust, he stated: "... I didn't -- I wasn't really sure specifically."

- When questioned about whether Medicaid trusts must be irrevocable or subject to recapture, Mr. DuBreuil stated: "I am not an expert."

- Interactions with Alberta was limited to overdrafts from checking.

- "I was not the broker of record at Wells Fargo."

Examination of the E. Alberta Veazey Analysis of Financial Transactions as submitted to Glasscock

Re:

E. Alberta Veazey

Analysis of Financial Transactions

Dear Robert,

Paragraph 1: DuBreuil Inserts Himself Between Jack, his Attorney and the Courts

DuBreuil States:

As requested, the following is a summary of selected assets and asset movement pertinent to

E. Alberta

Veazey’s personal assets and her assets of Alberta Veazey Family LLC. My research was

done at the request of Joseph J. “Jack” Beckett who is E. Alberta’s son and legal guardian. The final appointment of

guardianship became effective on 6/24/2011.

My research was done at the request of Joseph J. “Jack” Beckett - days prior a meeting was held where "they all" got together.

Attorneys, Jack, DuBreuil, Kristen, Warrington?

Analyst Commentary:

"selected assets and asset movement" - not comprehensive?

Analyst Commentary: It appears Mr. DuBreuil holds a misconception regarding the "her assets of Alberta Veazey Family LLC", seemingly

conflating it with the estate of Alberta.

Paragraph 2: DuBreuil's Libelious and Slanderious Statements to Delaware Courts

DuBreuil States:

In order to fulfill his duties as Alberta’s guardian Jack made a number of attempts, through you, as the

attoney for Mrs. Veazey’s guardianship, to contact Jack’s brother, Donald B. (“Don”) Veazey, who had held Mrs.

Veazey’s power of attorney, in order to make an orderly transfer of legal title of Alberta Veazey’s

assets [Account Zero] over to the

guardianship. Jack Beckett’s primary concerned was and remains how to assure that he can satisfy his mother’s

monthly nursing home bill (which approximates $6,000.00+/-month). From Jack Beckett’s perspective, Don

Veazey has ignored or refused all of Jack Beckett's requests to transfer legal title of Alberta Veazey’s financial

assets [Account Zero] to the guardianship.

Analyst Commentary:

Oblivious to Ryans numerous contacts with Thomas and the ongoing discussion of assets.

Analyst Commentary:

Fails to acknowledge Jack does not need my consent to move Alberta's assets and Jack has PoA both health and financial.

Analyst Commentary:

"ignored or refused to transfer legal title". DuBreuil cannot produce any document supporting his allegation. DuBreuil, aware

this document would be used in Delaware court in two weeks after sending, should be accutly aware of the liability this

statement brings his employer.

Regarding Contacts with Thomas: DuBreuil states that Jack Beckett made numerous attempts, through Thomas,

the attorney for Mrs. Veazey's guardianship, to contact Donald B. ("Don") Veazey. This statement obscures the fact

that Ryan had numerous contacts with Thomas, and all attorneys had ongoing discussions regarding Alberta's assets.

DuBreuil simply wasn't part of the overall conversation. DuBreuil's statement is misleading by omission.

Regarding Jack Beckett's Authority: DuBreuil fails to acknowledge the fact that Jack Beckett, as Alberta Veazey's

guardian, does not require my consent to transfer Alberta's assets. Furthermore, Jack Beckett holds Power of Attorney

for both health and financial matters of Alberta. This is a critical point of law and fact that DuBreuil omits.

Regarding "Ignored or Refused": DuBreuil alleges that "Don Veazey has ignored or refused all of Jack Beckett's

requests to transfer legal title of Alberta Veazey’s financial assets [Account Zero]

to the guardianship." This is a

false and defamatory statement. I and my attorney Ryan have not ignored or refused any legitimate requests. DuBreuil has

not provided, and cannot provide, any documentation to support this allegation. The opposite is supported in discovery.

This paragraph is a direct and damaging falsehood.

Regarding Awareness of Delaware Court Proceedings: DuBreuil was acutely aware that this statement would be used in

Delaware court proceedings within two weeks of its publication. This awareness amplifies the gravity of his false

statements and highlights the potential liability his employer faces due to his actions. He was not making an innocent

mistake, but rather making a calculated false statement.

In summary, DuBreuil has published false and unsupported statements. These statements are not only inaccurate

but also potentially defamatory and damaging, especially considering their intended use in a legal proceeding.

Paragraph 3: Misrepresentation of Assets

DuBreuil States:

"Alberta Veazey’s individual financial assets titled in her name appear to have been, as follows:

1) A Nationwide Annuity started on 12/22/2008 for $214,233.51

2) A brokerage account at Wells Fargo Advisers valued at $200,000 +/-.

3) Alberta’s share of the prcoeeds from a wrongful death lawsuit filed on behalf of her deceased husband

Samuel Veazey and valued at

$427,833.32 [Account Zero] as of 7/2009.

The total dollar value of the assets set forth above, as of the dates indicated, is $842,000 +/-. The dates and amounts

of the assets were derived from statements which Jack Beckett was able to obtain and provide to me."

Analyst Commentary: no item listed is an asset of Alberta's. the brokerage account at Wells Fargo Advisers

valued at $19,000. No account has ever existed representing Alberta's share of the mesothelioma lawsuit settlement.

DuBreuil also makes false statements about the nature of Alberta Veazey's assets. Specifically, DuBreuil

falsely represented the following:

- A Nationwide Annuity started on 12/22/2008 for $214,233.51" as an asset of Alberta Veazey.

- A brokerage account at Wells Fargo Advisers valued at $200,000 +/-." an asset of Alberta Veazey, when the account was actually valued at $19,000.

- Alberta’s share of the proceeds from a wrongful death lawsuit filed on behalf of her deceased husband Samuel Veazey and valued at $427,833.32 [Account Zero] as of 7/2009" as an asset of Alberta Veazey, when no such account representing Alberta's share of the mesothelioma lawsuit settlement ever existed.

In total, DuBreuil misrepresented that Alberta Veazey held assets with a total value of $842,000. The items listed by

DuBreuil are not assets of Alberta Veazey.

In summary, DuBreuil has published false and unsupported statements. These statements are not only inaccurate but also

potentially defamatory and damaging, especially considering their intended use in a legal proceeding.

Paragraph 4: DuBreuil's distorted view of his contact/interaction with Alberta and her family - like creepy distorted.

DuBreuil States:

The balance of this letter is a summary of my research, undertaken at Jack Beckett’s request, as to what has

happened to Alberta Veazey’s financial assets. Jack Beckett chose me to conduct this research because I was

Alberta’s banker and financial advisor while I was employed as a Sr. Financial Specialist at Wachovia Bank from

1/12/1999 to 5/7/2010; and, in that role, I had unique knowledge of the Alberta Veazey’s financial circumstances